GAJAMUDRA RESEARCH SERIES

How India's Fund Managers Think

Episode 002

The Diversification Myth

Why One Small Cap Fund Owns 105 Stocks While Another Places Bigger Bets on Fewer Ideas

Research Snapshot: 30 June 2026

Reading Time: ~10 Minutes

Every portfolio tells a story.

Behind every allocation is a decision.

Behind every decision is a belief.

Behind every belief is a fund manager trying to understand the future.

Welcome back to the Gajamudra Research Series, where we decode how India's mutual fund managers think—not by looking at returns, but by studying the portfolios they build.

Previously in Episode 001...

Yesterday, we discovered something that challenged one of the biggest assumptions about active investing.

We analysed 15 actively managed Small Cap mutual funds expecting to find 15 completely different portfolios.

Instead, we found surprising areas of agreement.

Three companies—

- Karur Vysya Bank

- Navin Fluorine International

- Craftsman Automation

appeared in nearly three-fourths of the portfolios we analysed.

Even more surprising...

Out of 521 companies, 254 were owned by just one mutual fund.

Some ideas united fund managers.

Others made them stand apart.

That left us with a much bigger question.

CHAPTER 1

If Two Fund Managers Like The Same Company...

...Why Don't They Invest The Same Amount?

Imagine two chefs preparing the same recipe.

Both choose the same ingredients.

Both use the same kitchen.

Both have years of experience.

Yet one adds a pinch of spice.

The other adds a handful.

Neither chef is wrong.

They're simply expressing different levels of confidence.

Small Cap fund managers do something remarkably similar.

In Episode 001, we discovered that many AMCs independently arrived at the same investment ideas.

But agreeing on what to buy is only half the story.

The more interesting question is...

How much of your investors' money are you willing to put behind that idea?

Because that's where conviction begins to reveal itself.

And that's exactly what today's episode is about.

🟨 GAJAMUDRA INSIGHT

Buying a company tells us what a fund manager likes.

The allocation tells us how strongly they like it.

Those are two very different conversations.

CHAPTER 2

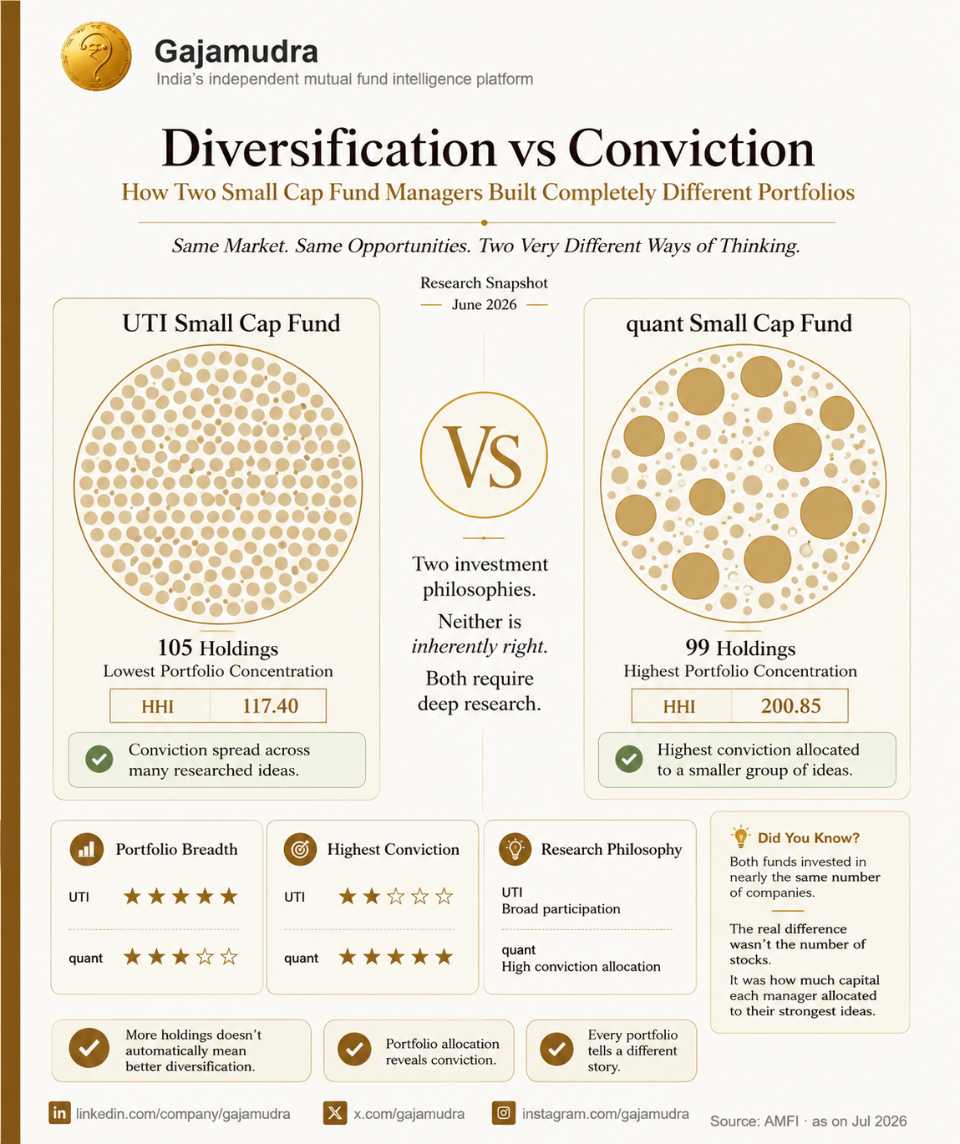

105 Stocks.

99 Stocks.

Which Portfolio Is Actually More Diversified?

Let's start with a simple thought experiment.

Imagine you're about to invest your life's savings.

You have only two choices.

Portfolio A

- Owns 105 companies.

Portfolio B

- Owns 99 companies.

Without knowing anything else...

which portfolio feels more diversified?

Most people instinctively answer:

Portfolio A.

It has more companies.

More companies should mean better diversification.

Right?

That's what many investors believe.

It's also what we expected before analysing the data.

But once we looked beneath the surface...

that assumption started to fall apart.

The First Impression

| Portfolio | Holdings |

|---|---|

| UTI Small Cap Fund | 105 |

| quant Small Cap Fund | 99 |

Question:

Which one do you think is more diversified?

At first glance...

the difference seems almost insignificant.

Just six companies.

Many investors would stop the analysis right there.

But here's what we discovered.

Counting holdings is like judging a book by the number of pages.

It tells you something.

But it doesn't tell you the whole story.

Because portfolios aren't just defined by how many companies they own.

They're defined by how capital is distributed across those companies.

And that's where everything changed.

CHAPTER 3

The Number Of Stocks Isn't The Real Story.

The Allocation Is.

This is one of the biggest misconceptions in investing.

People often ask:

"How many stocks does this mutual fund own?"

Far fewer ask:

"How much money has the fund manager invested in each one?"

That second question is often the more revealing one.

Imagine two portfolios, each holding 100 companies.

The first spreads its investments almost evenly across all 100 businesses.

The second also owns 100 companies...

but allocates a much larger share of its capital to just ten of its highest-conviction ideas.

On paper...

both portfolios own the same number of companies.

In reality...

they are expressing completely different investment philosophies.

One believes opportunity should be spread widely.

The other believes the strongest research deserves a larger allocation.

Neither approach is automatically better.

But they are fundamentally different ways of thinking about risk and opportunity.

📊 What Our Research Revealed

When we measured portfolio concentration instead of simply counting holdings, we found something fascinating.

🏆 UTI Small Cap Fund

- 105 holdings

- Lowest concentration score (HHI: 117.40)

🏆 quant Small Cap Fund

- 99 holdings

- Highest concentration score (HHI: 200.85)

Just six fewer companies.

Yet a completely different approach to allocating investors' money.

That was the moment we realised...

this wasn't a story about how many stocks fund managers owned.

It was a story about how they expressed conviction.

CHAPTER 4

Two Fund Managers.

One Market.

Two Completely Different Ways Of Thinking.

Imagine you ask two architects to design a school.

Both receive:

- The same land.

- The same budget.

- The same building materials.

- The same objective.

Yet one designs a wide campus with many smaller buildings.

The other creates a compact structure centered around a few larger buildings.

Neither architect is wrong.

They're simply solving the same problem differently.

That's exactly what we observed inside India's Small Cap mutual funds.

Every AMC studies the same economy.

The same listed companies.

The same quarterly results.

The same regulations.

And yet...

they often build remarkably different portfolios.

The Broad Builder

One portfolio immediately stood out for its breadth.

UTI Small Cap Fund held 105 companies, the highest among the fifteen funds we analysed.

More importantly, it also recorded the lowest portfolio concentration (HHI: 117.40).

That tells us something important.

The investment team wasn't simply adding more companies.

It was distributing capital more evenly across a larger set of researched businesses.

Think of it like planting an orchard instead of relying on a handful of trees.

If one tree has a difficult season, the orchard still has many others contributing to the harvest.

This doesn't mean the fund lacks conviction.

It means conviction is spread across many ideas rather than concentrated in a few.

For investors, that can provide broader exposure to opportunities across the Small Cap universe.

Portfolio Snapshot — UTI Small Cap Fund

- 105 Holdings

- Lowest HHI (117.40)

- Diversified allocation across companies

- Broad participation across researched ideas

Editorial callout:

"Conviction expressed through breadth."

The High-Conviction Builder

On the other side of our analysis was quant Small Cap Fund.

At first glance, it didn't appear dramatically different.

It owned 99 companies—only six fewer than UTI.

But when we looked deeper, the portfolio told a different story.

Among all fifteen funds, it recorded:

- The highest portfolio concentration.

- The highest Top-5 portfolio allocation.

- The highest Top-10 portfolio allocation.

In other words...

the research team chose to give greater importance to its strongest ideas.

Imagine you've spent months analysing hundreds of businesses.

Eventually, a handful stand out as exceptional.

A concentrated strategy says:

"If we truly believe these are our best ideas, they should have a greater influence on the portfolio."

Rather than spreading capital evenly, conviction becomes visible through larger allocations.

Portfolio Snapshot — quant Small Cap Fund

- 99 Holdings

- Highest HHI (200.85)

- Highest Top-5 allocation

- Highest Top-10 allocation

Editorial callout:

"Conviction expressed through concentration."

So...

Which Philosophy Is Better?

This is where many articles would try to declare a winner.

We won't.

Because the data doesn't support that conclusion.

Diversification and concentration are not opposing teams.

They're different portfolio construction philosophies.

A diversified portfolio aims to reduce dependence on any single company by spreading exposure across a wider set of opportunities.

A concentrated portfolio aims to let the strongest research ideas have a greater influence on outcomes.

Both approaches require rigorous research.

Both involve deliberate decision-making.

Both are valid expressions of active fund management.

The real takeaway isn't that one approach is superior.

It's that portfolio construction reveals how an investment team thinks—not just what it owns.

🟨 GAJAMUDRA INSIGHT

Many investors compare mutual funds using only returns.

But two funds with similar returns may have reached those outcomes through completely different philosophies.

One may have relied on broad diversification.

Another may have backed a handful of high-conviction ideas.

Understanding how a portfolio is built can be just as insightful as knowing how it performed.

CHAPTER 5

Then We Found A Fund That Refused To Look Like Everyone Else.

Every classroom has one student who solves the same maths problem...

using a completely different method.

The answer is correct.

The logic is sound.

But the approach surprises everyone.

We found something similar while analysing India's Small Cap mutual funds.

Most portfolios clustered around similar patterns.

Sector allocations differed...

Conviction levels differed...

Stock selections differed...

But one fund repeatedly appeared at the edge of our charts.

Not because it was better.

Not because it was worse.

Because it consistently thought differently.

That fund was quant Small Cap Fund.

Different Isn't Dangerous.

It's Deliberate.

One of the biggest misconceptions in investing is that if a portfolio looks different, it must also be riskier.

That's not always true.

Sometimes, a different-looking portfolio simply reflects a different research process.

Every fund manager studies the same economy.

The same inflation numbers.

The same interest rates.

The same company results.

Yet intelligent investment teams can arrive at completely different conclusions.

That's the essence of active fund management.

And quant Small Cap Fund was a great example of that.

Portfolio Personality

quant Small Cap Fund

🏆 Highest Portfolio Concentration

🏆 Highest Top-5 Allocation

🏆 Highest Top-10 Allocation

🏆 Highest Utilities Exposure

🏆 Highest Communication Services Exposure

🏆 Highest Cash Allocation

Editorial Callout

"A portfolio built around strong conviction rather than category averages."

The Market Is The Same.

The Conclusions Are Different.

Here's something we found fascinating.

While most AMCs allocated a significant portion of their portfolios to Industrials, quant Small Cap Fund had one of the lowest Industrials allocations in the category.

At the same time...

it stood out with comparatively higher exposure to sectors like Utilities and Communication Services.

That doesn't automatically make one approach better.

It simply tells us that the investment team saw opportunities where many others were less optimistic.

This is exactly why active management exists.

If every AMC reached the same conclusions...

every portfolio would eventually look identical.

Instead, each investment team brings its own research process, sector expertise and market outlook to the table.

A Portfolio Isn't Just Built.

It's Designed.

Think of a mutual fund portfolio like a football team.

Every coach wants to win.

But no two coaches select the exact same starting eleven.

Some build around a strong defence.

Others trust attacking talent.

Some prefer experienced players.

Others back young potential.

The objective is identical.

The strategy isn't.

Portfolio management works in much the same way.

Every AMC wants to create long-term wealth for its investors.

How they attempt to achieve that goal is what makes each portfolio unique.

🟨 GAJAMUDRA INSIGHT

When investors compare mutual funds, they often focus on one number:

Returns.

But returns are the final score.

Portfolio construction is the game plan.

If you only look at the scoreboard...

you'll never understand the strategy that produced it.

Studying portfolios gives us something far more valuable than performance.

It gives us insight into how India's fund managers think.

CHAPTER 6

The Quiet Decisions That Most Investors Never Notice.

When people discuss mutual funds...

they usually talk about:

- Which stocks were bought.

- Which sectors were overweight.

- Which fund performed the best.

But during our research, we realised something.

Some of the most interesting decisions weren't about what fund managers bought.

They were about what they chose not to buy.

Or even...

what they chose to wait for.

That's where the next layer of this investigation begins.

Because one overlooked number quietly revealed how differently India's fund managers were preparing for the future.

And surprisingly...

it wasn't a stock at all.

It was cash.